Loan settlement can feel like standing at the edge of a financial cliff with a phone in one hand and a pile of statements in the other. The good news: settlement is not magic, and it is not chaos. It is a negotiation. When you understand how lenders think, what rights you have, what paperwork matters, and which loan repayment options may work better than settlement, you can move from panic to plan.

This guide focuses on the U.S. context and practical best practices for consumers dealing with personal loans, credit cards, medical debt, some private student loans, auto deficiencies, and other consumer debts. It is educational, not legal, tax, or financial advice. If you are facing a lawsuit, foreclosure, repossession, wage garnishment, bankruptcy decision, or large tax issue, speak with a qualified attorney or tax professional in your state.

First, understand what loan settlement really means

Loan settlement means a creditor or debt collector agrees to accept less than the full balance owed as satisfaction of the debt. In plain English: you pay an agreed amount, and the other side agrees not to keep pursuing the remaining balance.

That sounds simple, but the details matter. A successful settlement is not just “I sent money and they stopped calling.” A successful settlement should include:

- A written agreement before you pay.

- The exact debt being settled.

- The exact amount you must pay.

- The payment deadline or installment schedule.

- A statement that the payment resolves the account.

- Any promises about stopping collection activity.

- How the account will be reported, if the creditor or collector reports to credit bureaus.

- A plan for tax paperwork, if canceled debt may be reported.

Settlement is different from normal repayment. Repayment means you are paying what you owe according to the original contract or a modified plan. Settlement usually means the creditor is forgiving part of the balance. The IRS generally treats forgiven or canceled debt as income unless an exception or exclusion applies, such as bankruptcy or insolvency, so tax planning should be part of your settlement strategy rather than an afterthought. (irs.gov)

Why lenders agree to settle

A bank, lender, or collection agency usually settles because it believes settlement is the most practical way to recover money. If the account is seriously delinquent, the creditor may be weighing options such as continued collection, charge-off, selling the debt, suing, or accepting a reduced payment now.

A lender’s decision can depend on factors like:

- How far behind the account is.

- Whether the debt is secured or unsecured.

- Whether the lender believes you can pay more.

- Whether you have income, assets, or hardship documentation.

- Whether the account has been charged off or sent to collections.

- Whether a lawsuit has already been filed.

- The lender’s internal policies.

- State law and the age of the debt.

Here is the guru truth: settlement is rarely about who sounds the most desperate. It is about documentation, timing, risk, and clarity. Your job is to show that your offer is realistic, available, and better than the alternative.

Bank loan settlement rules: what actually governs the process?

People often search for bank loan settlement rules expecting one universal U.S. rulebook. There is no single national rule that forces every bank to settle every loan for a certain percentage. Settlement policies vary by creditor, loan type, contract, account status, and state law.

That said, several rules and consumer protections shape the settlement process:

- Debt validation rules: If a debt collector contacts you, they generally must provide validation information about the debt, including details that help you identify it and instructions for disputing it. CFPB rules explain that collectors must provide validation information either in the initial communication or in writing or electronically shortly after. (consumerfinance.gov)

- Fair debt collection rules: Debt collectors cannot harass, oppress, abuse, or deceive you when collecting a debt. The FDCPA and Regulation F address issues such as repeated calls meant to harass, false statements, certain third-party communications, and inconvenient communication methods. (consumerfinance.gov)

- Time-barred debt rules: Statutes of limitation vary by state and debt type. The CFPB warns that making a partial payment or acknowledging an old debt may restart the limitations period in some circumstances, so be careful before paying or promising to pay old accounts. (consumerfinance.gov)

- Debt relief company rules: Many for-profit debt settlement companies that sell services by phone are covered by the FTC’s Telemarketing Sales Rule. The FTC says covered companies cannot collect fees before they have settled or otherwise resolved a debt, and the CFPB describes specific conditions that must occur before a debt settlement company may charge certain fees. (ftc.gov)

- Tax rules: Canceled debt may be taxable, and certain creditors may issue Form 1099-C when $600 or more of debt is canceled after an identifiable event. A missing Form 1099-C does not automatically mean the canceled debt is tax-free. (irs.gov)

- Credit reporting rules: Negative information generally may remain on a credit report for up to seven years, while bankruptcy may remain for up to ten years. A paid or settled collection should generally show a zero balance if it is reported. (consumerfinance.gov)

So, when you think about bank loan settlement rules, think in layers: your contract, the creditor’s policies, federal collection rules, state law, tax rules, credit reporting rules, and any lawsuit deadlines.

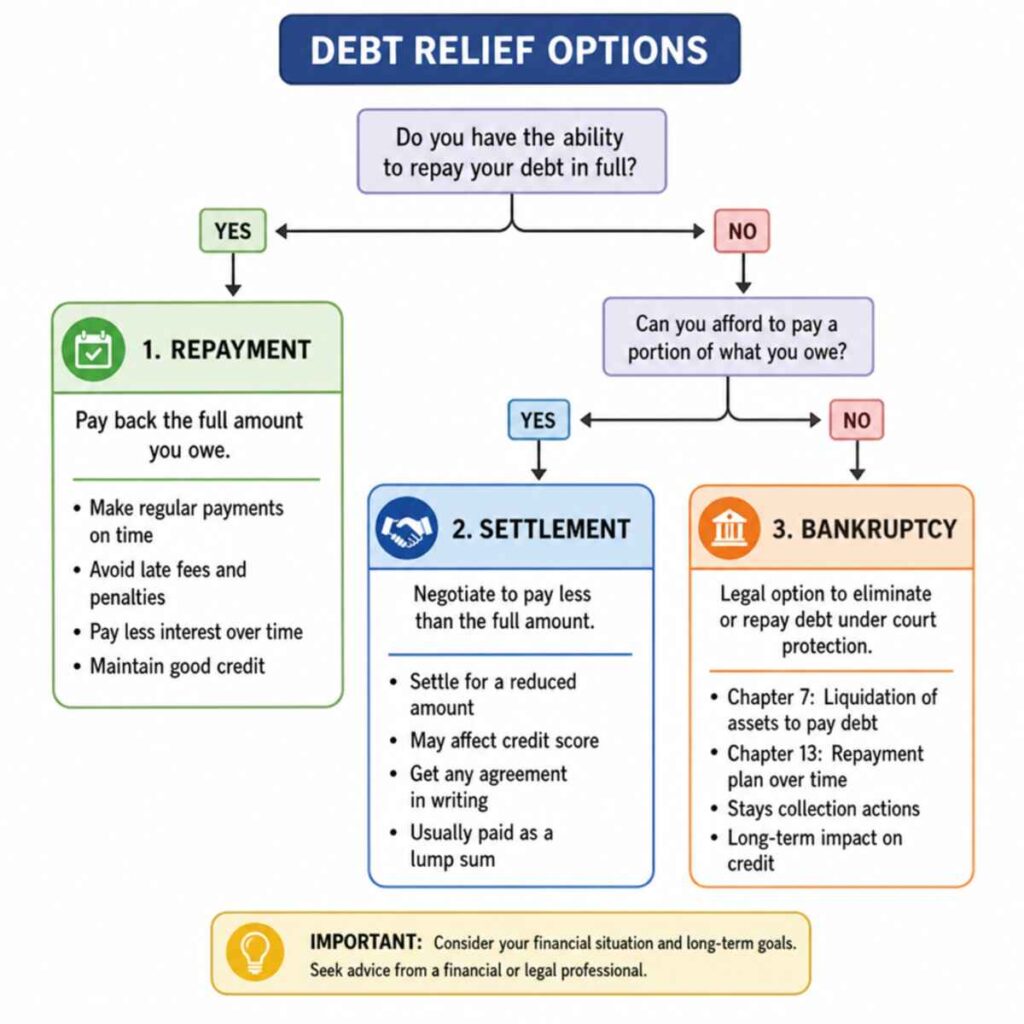

Settlement is not always the best debt relief option

Settlement can be powerful, but it is not always the cleanest or cheapest path. Before you push for a reduced payoff, compare your debt relief options carefully.

Settlement may make sense when:

- You cannot afford the current payments.

- You have a legitimate hardship.

- The debt is unsecured or no collateral is at immediate risk.

- You can offer a lump sum or short installment plan.

- The account is already delinquent or in collections.

- Bankruptcy would be too severe or unnecessary for your situation.

- You understand the tax and credit consequences.

Settlement may be risky when:

- You are current and can afford a modified repayment plan.

- The debt is secured by a car, home, or other property you want to keep.

- You are being sued and do not have legal advice.

- The debt may be time-barred.

- You are relying on a company that wants upfront fees.

- You are draining emergency savings or retirement funds to settle.

- You are settling one account while ignoring more urgent debts.

The big idea: settlement is one tool. It is not the whole toolbox.

Start with a full debt inventory

Before you negotiate, make a debt inventory. This step is not glamorous, but it is where settlement success begins. You cannot negotiate well if you do not know what you owe, who owns it, or what you can realistically pay.

Create a simple list with:

- Creditor or collector name.

- Original creditor name, if different.

- Account number or partial account number.

- Current balance.

- Past-due amount.

- Interest rate, if known.

- Last payment date.

- Current account status.

- Whether the debt is secured or unsecured.

- Whether you have received collection letters.

- Whether you have been sued.

- Whether the debt appears on your credit reports.

- Your best estimate of what you can offer.

You can review your credit reports to help identify accounts, but remember that not every debt appears on a credit report. Creditors are not required to report every account to credit reporting companies. (consumerfinance.gov)

Use the official free credit report source, not a look-alike site. AnnualCreditReport.com states that it is the only official site directed by federal law for free credit reports, and CFPB resources note that consumers can request free weekly reports from the major credit reporting companies. (annualcreditreport.com)

Know which debts to prioritize

Not all debts have the same urgency. A calm strategy protects your household first, then handles creditors in the right order.

Generally, prioritize:

- Housing: Rent, mortgage, property taxes, utilities, and anything tied to keeping your home stable.

- Transportation: Car payments or insurance if you need the vehicle for work, caregiving, or medical needs.

- Court deadlines: Lawsuits, judgments, garnishment notices, and hearing dates.

- Secured debts: Loans tied to collateral, such as auto loans or home equity loans.

- High-risk unsecured debts: Accounts close to lawsuit activity or aggressive collection.

- Lower-risk unsecured debts: Older debts, small balances, or accounts not currently in active legal collection.

This does not mean unsecured debts are unimportant. It means your settlement plan should not create a bigger crisis. Do not settle a credit card if doing so makes you miss rent. Do not settle a personal loan if it leaves you unable to buy medication. Financial peace starts with survival math.

Review loan repayment options before negotiating settlement

Settlement often works best after you have considered less damaging loan repayment options. If you still have a relationship with the original lender, ask about hardship programs before the account moves deeper into collections.

Possible repayment options include:

- Hardship plan: Temporary reduced payments because of job loss, illness, divorce, reduced hours, or other hardship.

- Interest rate reduction: A lower rate that makes the monthly payment manageable.

- Fee waiver: Removal or suspension of late fees or penalty fees.

- Extended repayment: More time to repay, often with a lower monthly payment.

- Forbearance: Temporary pause or reduction in payments, often used during short-term hardship.

- Deferment: Payment postponement, common in some student loan and hardship contexts.

- Debt management plan: A nonprofit credit counseling agency may help you make one monthly payment to the agency, which then pays creditors. These plans typically aim to lower monthly payments, interest, or fees rather than erase the debt. (consumerfinance.gov)

- Consolidation loan: A new loan that pays off multiple debts, leaving one payment. This can help if the new terms are genuinely better, but it can backfire if fees, rates, or longer repayment increase the total cost.

- Income-driven repayment for federal student loans: Federal Student Aid provides repayment plan information and tools such as Loan Simulator. Because federal student loan rules and plan availability can change, borrowers should verify current options directly with Federal Student Aid before choosing a strategy. (studentaid.gov)

If a repayment option keeps you current, protects your credit, and fits your budget, it may be wiser than settlement. If repayment only delays the inevitable, settlement may deserve a closer look.

Understand secured vs. unsecured loans

This is one of the most important distinctions in settlement.

Unsecured debt

Unsecured debt is not tied to specific collateral. Common examples include:

- Credit cards.

- Personal loans.

- Medical bills.

- Some private student loans.

- Certain lines of credit.

Unsecured debts are often more likely to be considered for settlement because the creditor cannot simply repossess collateral. However, the creditor may still report delinquency, sell the debt, hire collectors, or sue.

Secured debt

Secured debt is tied to property. Common examples include:

- Auto loans.

- Mortgages.

- Home equity loans or lines of credit.

- Some secured personal loans.

With secured loans, settlement can be more complicated because the lender may have rights to repossess or foreclose on the collateral if you default. If your car or home is involved, ask about loss mitigation, modification, reinstatement, redemption, refinance, sale, or surrender options before assuming settlement is the right move.

If a secured asset is essential to your life, do not negotiate casually. Get advice before missing payments or accepting terms you do not fully understand.

Prepare your hardship story, but keep it factual

A settlement conversation is not a confession booth. You do not need to share every painful detail of your life. You do need to explain why the original payment terms no longer work and why your offer is realistic.

A strong hardship explanation includes:

- What changed.

- When it changed.

- How it affected income or expenses.

- What you can afford now.

- Whether the hardship is temporary or long-term.

- Why your settlement offer is the best available solution.

Examples of hardship include:

- Job loss.

- Reduced hours.

- Medical expenses.

- Disability.

- Divorce or separation.

- Death of a household earner.

- Business closure.

- Natural disaster.

- Caregiving responsibilities.

- Major increase in essential expenses.

Keep the tone respectful and firm. You are not begging. You are presenting a financial reality.

Calculate what you can actually pay

The number you offer should come from your budget, not from wishful thinking. A lender may push for more, but if more is impossible, a bigger promise only creates a second failure.

Start with three numbers:

- Your survival number: The amount you need monthly for housing, food, utilities, transportation, insurance, medical needs, childcare, and minimum obligations.

- Your safe settlement fund: Money you can use without missing essentials or emptying every emergency dollar.

- Your maximum offer: The highest amount you can pay without causing a new crisis.

If you have a lump sum, know the exact amount and when it is available. If you need installments, know the exact monthly amount and how long you can sustain it. Many settlements fail because the borrower agrees to an installment plan that looked possible for one month but impossible for six.

A smart offer is not always the lowest offer. It is the lowest offer that has a realistic chance of acceptance and completion.

Should you stop paying to force a settlement?

This is one of the most dangerous questions in debt negotiation.

Some creditors will not consider settlement while an account is current. That leads some borrowers to intentionally stop paying. But missed payments can trigger late fees, credit damage, collection calls, charge-off, lawsuits, repossession risk for secured debt, and stress. Debt settlement companies sometimes tell consumers to stop paying creditors, but the CFPB warns that many lenders do not negotiate with debt settlement companies and that debt settlement can be risky. (consumerfinance.gov)

Before stopping payments, ask yourself:

- Can I afford the consequences if settlement fails?

- Is this debt secured by property I need?

- Is there a hardship plan available instead?

- Could a nonprofit credit counselor help?

- Am I close to being sued?

- Is bankruptcy a better protection?

- Do I understand the tax impact of forgiven debt?

The Writing Guru rule: never create delinquency without a plan, a timeline, and a backup option.

Contact the right party

Who you negotiate with depends on where the debt is in its life cycle.

If the account is still with the original lender

Call the lender’s hardship, loss mitigation, recovery, or collections department. Front-line customer service may not have authority to settle. Ask directly:

- “Which department handles settlement or hardship arrangements?”

- “Is this account eligible for a settlement review?”

- “Do you require hardship documentation?”

- “Will you send terms in writing before payment?”

If the account is with a debt collector

First confirm the debt. Debt collectors generally must provide validation information, and if you dispute the debt in writing during the validation period, the collector must pause collection of the disputed debt until verification is provided. (consumerfinance.gov)

Ask:

- “Do you own this debt or are you collecting for someone else?”

- “Who is the current creditor?”

- “What is the original creditor?”

- “What is the full balance?”

- “Do you have authority to settle?”

- “Will you provide the settlement agreement in writing before I pay?”

If a lawsuit has been filed

Do not ignore it. A settlement conversation does not replace a legal response. If you miss court deadlines, the creditor may be able to seek a default judgment. Talk to a consumer debt defense attorney, legal aid office, or court self-help center as soon as possible.

Use a simple negotiation script

You do not need fancy words. You need clarity.

Try this:

“I’m calling about account ending in . I’m experiencing financial hardship and cannot afford the current balance or payment terms. I want to resolve the account if we can agree on a realistic settlement. I can pay $ by _____. If accepted, I need a written agreement stating that this payment settles the account and that the remaining balance will not be pursued.”

If they say no, ask:

“What amount would you be authorized to accept to resolve the account?”

If the number is too high:

“I understand. I don’t have access to that amount. My maximum available amount is $_____. If that is not acceptable today, can you note the account and tell me when I may check back?”

If they push for a payment before sending terms:

“I’m willing to pay once I receive the agreement in writing and confirm the terms. I cannot make a payment without written settlement terms.”

Calm repetition is your friend. You are not there to win an argument. You are there to reach a documented agreement.

What to include in a settlement agreement

Never rely on “Trust me, it’s in the notes.” Notes are not a settlement agreement. Before paying, get written terms you can save.

Your settlement letter or agreement should include:

- Your name.

- Creditor or collector name.

- Original creditor, if applicable.

- Account number or partial account number.

- Current balance.

- Settlement amount.

- Due date or installment schedule.

- Payment method.

- Statement that the settlement amount resolves the account.

- Statement that the remaining balance will be forgiven, canceled, or not pursued.

- Statement that collection activity will stop after completed payment.

- Any credit reporting language offered.

- Signature, letterhead, or other proof of authority.

- Contact information for the company.

If the agreement is missing the “remaining balance” language, ask for clarification. You do not want to pay a reduced amount only to have the unpaid portion sold or collected later. Regulation F prohibits a debt collector from selling, transferring for consideration, or placing for collection a debt if the collector knows or should know it has been paid, settled, or discharged in bankruptcy. (consumerfinance.gov)

Be careful with payment methods

Once you have written terms, pay in a way that creates proof and limits risk.

Consider:

- Cashier’s check.

- Money order.

- Bill pay from your bank.

- A separate account used only for settlement payments.

- Debit card only if you understand authorization terms.

Be cautious with:

- Giving direct access to your main checking account.

- Open-ended automatic withdrawals.

- Paying before the agreement is in writing.

- Sending money to an individual instead of the company.

- Payment apps with weak dispute protection.

- Pressure to pay immediately using gift cards, crypto, wire transfer, or unusual methods.

After payment, save:

- The settlement agreement.

- Proof of payment.

- Confirmation number.

- Names of representatives.

- Dates and times of calls.

- Any final “paid” or “settled” letter.

Your future self may need these documents if the account is sold by mistake, reported incorrectly, or questioned during a mortgage application.

Watch out for tax consequences

Here is the part many people discover too late: the amount forgiven in a settlement may count as taxable income. For example, if you owe $10,000 and settle for $4,000, the $6,000 forgiven may be cancellation-of-debt income unless an exception or exclusion applies.

The IRS explains that canceled debt is generally included in income unless an exception or exclusion applies. It also explains exclusions such as bankruptcy and insolvency. Insolvency generally means your total liabilities were more than the fair market value of your assets immediately before the cancellation, but the calculation can be technical. (irs.gov)

Important tax tips:

- Ask whether the creditor expects to issue Form 1099-C.

- Do not assume “no form” means “no tax issue.”

- Keep the settlement letter and payment proof.

- If you receive Form 1099-C, review it for accuracy.

- If you were insolvent, ask a tax professional about Form 982.

- If the debt was discharged in bankruptcy, ask how the bankruptcy exclusion applies.

Tax planning does not mean settlement is bad. It means the real cost of settlement is not just the check you write to the creditor.

Understand credit reporting after settlement

Settlement can help close a chapter, but it does not erase the credit history that came before it. Late payments, charge-offs, and collections may remain if they are accurate and within the reporting period. The CFPB says credit reporting companies generally may report negative account payment history for up to seven years, and accurate negative information generally cannot be removed just because it is unfavorable. (consumerfinance.gov)

A settled account may be reported with language such as:

- Settled.

- Settled for less than full balance.

- Paid settlement.

- Paid collection.

- Zero balance.

If a collection account was reported and then settled, it should generally reflect a zero balance. (consumerfinance.gov)

After settlement, check your credit reports. If the balance is wrong, the account appears multiple times incorrectly, or the account is still shown as actively owed after the settlement is complete, dispute the error with the credit reporting company and the furnisher. The CFPB notes that consumers can dispute inaccurate information themselves at no cost. (consumerfinance.gov)

Debt settlement companies: help or hazard?

Some people settle debts themselves. Others hire a debt settlement company. Before you pay for help, understand the risk.

A legitimate professional should explain fees, risks, timelines, tax consequences, and credit impact. A risky company may promise quick results, tell you to stop paying without explaining consequences, charge improper upfront fees, or imply that every creditor will accept a steep discount.

The FTC says covered debt relief companies cannot collect fees before they settle or otherwise resolve a customer’s debts, and they must disclose key information such as cost, timing, and possible negative consequences. (ftc.gov)

Red flags include:

- “Guaranteed” settlement results.

- Upfront fees before any debt is resolved.

- Pressure to sign immediately.

- Advice to ignore lawsuits or court papers.

- Claims that credit damage will disappear quickly.

- Refusal to explain tax consequences.

- Refusal to say whether your money stays under your control.

- No clear cancellation policy.

- No written fee schedule.

Under CFPB guidance, money saved in an account for use by a debt settlement company still belongs to the consumer, must be administered by an independent third party, must remain under the consumer’s control, and must be withdrawable without penalty. (consumerfinance.gov)

Compare debt relief options before choosing

Let’s walk through common debt relief options in practical language.

Do-it-yourself negotiation

Best for people who are organized, comfortable making calls, and able to keep records. You avoid company fees and stay in control. The challenge is that you must handle creditor communication, documentation, and follow-up yourself.

Nonprofit credit counseling

Best for people who can repay debt with better structure, lower interest, or waived fees. Credit counseling organizations are usually nonprofits that help with budgeting, money management, and debt management plans. They do not erase debt, but they may help make repayment more manageable. (consumerfinance.gov)

Debt management plan

Best for credit card or unsecured debt where interest is the main problem and you can afford a monthly payment. You make one payment to the counseling agency, and the agency pays creditors. This is not the same as settlement because the goal is usually repayment, not partial forgiveness.

Debt consolidation

Best when you qualify for a lower interest rate or simpler payment without extending yourself dangerously. It is risky if you consolidate, keep using credit cards, and end up with both the new loan and new balances.

Hardship program

Best when your financial setback is temporary and the lender is willing to modify payments. This can be less damaging than settlement if it prevents delinquency.

Bankruptcy

Best when debts are overwhelming, lawsuits are active, wages may be garnished, or settlement is not realistic. Bankruptcy has serious consequences, but it also provides legal protections that settlement does not. The U.S. Trustee Program explains that individuals generally must complete approved credit counseling before filing bankruptcy, with limited exceptions, and debtor education after filing to receive a discharge. (justice.gov)

Legal aid or consumer attorney

Best when you have been sued, threatened with garnishment, contacted about old debt, or confused about state law. Settlement without legal advice can be costly if you accidentally revive a time-barred debt or miss a court deadline.

The best option is not the one that sounds easiest. It is the one that solves the most risk with the least long-term damage.

Special situation: old or time-barred debt

Old debt requires extra caution. A debt may be too old for a collector to sue under your state’s statute of limitations, but that does not always mean collectors must stop asking for payment. The CFPB explains that in many states collectors may still attempt to collect time-barred debt, but they cannot sue or threaten to sue if the statute of limitations has passed. (consumerfinance.gov)

Before negotiating old debt:

- Find the date of last payment.

- Check your records.

- Review the validation notice.

- Learn your state’s statute of limitations.

- Do not acknowledge the debt casually.

- Do not make a small “good faith” payment without advice.

- Consult an attorney if you are unsure.

This is one area where a $25 payment can become a very expensive mistake if it restarts the clock under applicable law.

Special situation: military servicemembers

If you are on active duty or recently served, review protections under the Servicemembers Civil Relief Act. The CFPB states that the SCRA can allow the interest rate on certain pre-service loans to be reduced to 6 percent, and servicemembers must notify the lender in writing and include appropriate documentation during active duty or within the stated post-service window. (consumerfinance.gov)

That protection is not the same as settlement, but it may change your repayment strategy. If a rate reduction makes the payment affordable, it may be better than trying to settle.

Special situation: co-signed or joint loans

Settlement can affect more than one person. If a parent, spouse, partner, friend, or business associate co-signed the loan, the creditor may still pursue the co-signer unless the settlement agreement releases everyone liable.

Before settling a co-signed or joint debt, ask:

- Who is legally responsible?

- Will the settlement release all borrowers?

- Will the creditor report the account on both credit reports?

- Could the co-signer be sued for the remaining balance?

- Does the agreement name every released party?

Do not assume your settlement protects the other person. Get it in writing.

Special situation: debt already in court

If you have been sued, settlement is still possible, but the process needs more precision.

Ask for any agreement to address:

- Whether the lawsuit will be dismissed.

- Whether dismissal will be with prejudice or without prejudice.

- Whether a judgment will be entered.

- Whether payments are required before dismissal.

- What happens if you miss an installment.

- Whether the creditor can seek the full balance after default.

- Whether court costs or attorney fees are included.

A settlement after a lawsuit can be useful, but a bad court settlement can create a judgment faster than you expected. Get legal advice if possible.

A practical pre-settlement checklist

Before making an offer, complete this checklist:

- I know who currently owns or collects the debt.

- I have requested or reviewed validation information if a collector contacted me.

- I know whether the debt is secured or unsecured.

- I checked whether a lawsuit has been filed.

- I reviewed my income and essential expenses.

- I know my maximum affordable offer.

- I considered hardship programs and other loan repayment options.

- I understand possible tax consequences.

- I understand possible credit reporting consequences.

- I know whether the debt may be time-barred.

- I have a plan to get the agreement in writing before paying.

- I have a safe payment method.

- I will keep every document.

If you cannot check these boxes yet, pause. Preparation is cheaper than regret.

How to make your offer stronger

Creditors hear vague promises all day. Make your offer concrete.

A stronger offer sounds like:

“I can pay $2,000 by August 15 if you agree in writing that this amount settles the account in full and the remaining balance will not be pursued.”

A weaker offer sounds like:

“I might be able to send something soon if you can help me out.”

To strengthen your position:

- Offer a specific amount.

- Offer a specific date.

- Explain the hardship briefly.

- Be honest about limits.

- Avoid emotional over-explaining.

- Ask for written approval.

- Stay polite even if the answer is no.

- Keep notes after every call.

If the creditor rejects your first offer, do not panic. Ask what they can accept, compare it to your maximum, and decide whether to counter, wait, or explore other options.

What not to say during negotiation

Words matter. Avoid statements that weaken your position or create legal risk.

Be careful with:

- “I can borrow from my retirement account.”

- “My family can probably give me more.”

- “I know I owe it, I just don’t want to pay.”

- “I’ll pay something today even without a letter.”

- “I don’t care about taxes.”

- “I’ll agree to whatever stops the calls.”

- “You can debit my account whenever.”

Better phrases:

- “This is the maximum amount available.”

- “I need written terms before payment.”

- “I am not able to authorize automatic withdrawals.”

- “Please send the agreement for review.”

- “I need time to evaluate whether this is affordable.”

You are allowed to slow the conversation down.

Keep communication records like a pro

Your settlement file should be boring, complete, and easy to understand. That is exactly what makes it powerful.

Keep:

- Original loan documents, if available.

- Monthly statements.

- Collection letters.

- Validation notices.

- Emails.

- Call logs.

- Names and ID numbers of representatives.

- Settlement offers.

- Final agreement.

- Payment proof.

- Credit report screenshots or PDFs.

- Tax forms.

The CFPB advises consumers dealing with collectors to keep letters and messages and make copies of communications they send. (consumerfinance.gov)

A good record turns “I thought we settled this” into “Here is the agreement and proof of payment.”

After you pay: do not disappear

Settlement is not finished the moment money leaves your account. You need closure.

After payment:

- Confirm the payment cleared.

- Request a final paid or settled letter.

- Save proof in multiple places.

- Monitor mail and email for additional notices.

- Review credit reports after the creditor has had time to update.

- Dispute inaccurate reporting if necessary.

- Watch for Form 1099-C during tax season.

- Keep the file permanently, or at least for several years.

If another collector contacts you about the same settled debt, send a copy of the settlement proof and payment confirmation. Do not pay twice because someone’s database failed.

If the bank refuses to settle

A refusal is not the end of your strategy. It simply means that settlement is not available on the terms you offered at that moment.

Ask:

- “Is there a hardship program?”

- “Can payments be reduced temporarily?”

- “Can interest or fees be reduced?”

- “Is there a different department that reviews settlements?”

- “When may I request another review?”

- “What documentation would help?”

If you believe a national bank or federal savings association treated you unfairly or mishandled your issue, the OCC says consumers should try to resolve the issue directly with the bank first and may file a complaint with the OCC if the institution is under its jurisdiction. (helpwithmybank.gov)

You can also submit complaints about many consumer financial products or services to the CFPB, particularly when dealing with debt collection, credit reporting, loans, or servicing issues.

Common mistakes that derail settlement success

Avoid these traps:

Paying without written terms

This is the classic mistake. A verbal promise is not enough.

Offering money you cannot afford

A failed settlement can leave you with less cash and the same debt problem.

Ignoring taxes

Canceled debt can create a tax bill. Plan early.

Forgetting about co-signers

If another person is liable, make sure the settlement protects them too.

Settling the wrong debt first

Do not use limited cash on a low-risk account while a lawsuit or secured loan crisis grows.

Trusting unrealistic promises

No one can guarantee every creditor will settle or that accurate negative credit history will vanish.

Missing court deadlines

Settlement talks do not pause a lawsuit unless the court process or written agreement says so.

Reviving old debt accidentally

Old debts require caution because payment or acknowledgment can affect the statute of limitations in some states. (consumerfinance.gov)

Failing to check credit reports

A settlement should generally show the account as resolved or zero balance if reported. Verify and dispute errors.

A 30-day settlement action plan

If you are ready to move from overwhelm to action, use this plan.

Days 1 to 3: Gather documents

Collect statements, collection letters, credit reports, court papers, income proof, hardship proof, and your budget.

Days 4 to 7: Build your debt inventory

List every account. Mark urgent debts, secured debts, lawsuit risks, and accounts you may want to settle.

Days 8 to 10: Review alternatives

Call lenders about hardship programs. Contact a nonprofit credit counselor if repayment may still be possible. Consider legal advice if lawsuits, old debts, or secured property are involved.

Days 11 to 15: Choose your target accounts

Pick the debts where settlement makes the most sense. Do not scatter small offers everywhere unless that is part of a deliberate plan.

Days 16 to 20: Make first contact

Call the correct department or collector. Confirm authority, account details, and whether settlement is available. Take notes.

Days 21 to 25: Negotiate terms

Make specific offers. Ask for written agreements. Do not authorize payment until terms are clear.

Days 26 to 30: Pay and document

Pay according to the agreement. Save proof. Request final confirmation. Calendar follow-up dates for credit report review and tax paperwork.

Thirty days may not solve every debt. But thirty focused days can replace confusion with momentum.

Quick settlement success checklist

Use this before every payment:

- The agreement is in writing.

- The company name matches the creditor or authorized collector.

- The account number matches my records.

- The settlement amount is exact.

- The due date is exact.

- The agreement says the remaining balance will not be pursued.

- I understand whether installments are allowed.

- I know what happens if a payment is late.

- I understand possible tax consequences.

- I have a safe payment method.

- I saved a copy of everything.

If any item is missing, ask questions before paying.

Frequently asked questions

Can I negotiate a loan settlement myself?

Yes, many consumers negotiate directly with creditors or collectors. The key is to confirm the debt, know your budget, make a realistic offer, get written terms, and keep proof. If the debt is old, secured, disputed, or in court, consider legal advice first.

Will a bank settle a loan if I am current?

Sometimes, but many lenders are less likely to settle an account that is current because they still expect full repayment. Ask about hardship programs and other loan repayment options before considering delinquency.

Is settlement better than a debt management plan?

Not always. Settlement may reduce the balance but can damage credit and create tax issues. A debt management plan usually focuses on structured repayment through a credit counseling agency and may reduce interest or fees without forgiving principal. (consumerfinance.gov)

How much should I offer?

There is no universal percentage that works for every creditor. Base your offer on your real budget, the age and status of the account, whether the debt is secured, and what you can pay by the deadline. Avoid promising more than you can complete.

Can a debt collector keep calling after I ask them to stop?

You have rights around collector communications. Debt collectors cannot harass, abuse, or deceive you, and Regulation F includes rules about communication methods and opt-outs for electronic communications. You can also use written requests and sample letters to manage collector contact. (consumerfinance.gov)

Will settlement remove the account from my credit report?

Usually, no. Accurate negative information can generally remain for the allowed reporting period. Settlement may update the balance to zero or show the account as settled, but it does not automatically delete prior late payments, charge-offs, or collections. (consumerfinance.gov)

What if I cannot afford even a settlement?

Look at broader debt relief options: hardship plans, nonprofit credit counseling, legal aid, bankruptcy consultation, or state and local assistance programs. If you truly cannot pay, do not let shame push you into an impossible agreement.

Final guidance: settlement success is built on clarity

Loan settlement success does not come from being aggressive, frightened, or lucky. It comes from being prepared.

Know the debt. Know your rights. Know your budget. Know the alternatives. Get every promise in writing. Protect yourself from tax surprises. Follow up after payment. And if the situation is legally complicated, get professional guidance before signing or paying.

The wisest settlement is not always the biggest discount. It is the agreement you can complete, document, and recover from with confidence.